Call Us Today (800) 229-5266

Based on an article written by our insurance partners, Ironpeak®.

According to the Small Business Administration (SBA), there is currently over 33 million small businesses in the United States, 19 million of which operate as home-based companies, including many insurance agents or small agencies.

Starting a home-based business is exciting, challenging, and can offer many benefits, such as greater flexibility and lower overhead costs. However, along with the benefits, potential risks can ruin a new business.

In this article, we share how agents can inform their clients about the importance of having home-based business insurance, who needs these policies, and the types of coverages business owners might need to help them protect their assets and ensure a good night’s sleep.

Inform Your Clients about Home-Based Business Insurance

With all the challenges small business owners face and the decisions they must make, insurance often seems like a low priority and an area in which they have limited knowledge or experience. Consequently, many owners of home-based businesses assume that their homeowner’s policy would adequately cover their business. This is where SeibertKeck Insurance Partners can truly add value. We help business owners understand the risks they may not even realize they’re exposed to—and offer tailored insurance solutions to protect what they’ve worked so hard to build.

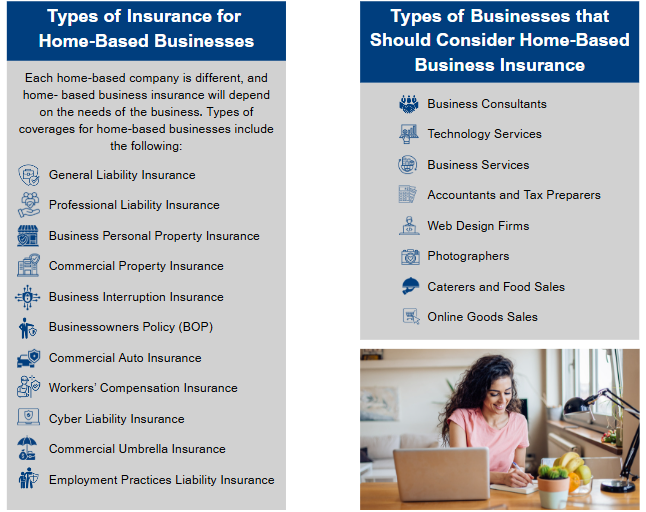

What is Home-Based Business Insurance?

First and most importantly, home-based business insurance is NOT a part of a homeowner’s policy which does not typically provide the coverages that a home- based business needs. A standard home insurance policy may only cover a limited amount for business property, or some homeowners’ policies might not cover business-related items at all.

Home-based business insurance is a group of coverages created for business owners who operate out of their homes. The policy covers unforeseen costs associated with owning a business, such as property damage, legal fees, loss of business income, employee injuries, or data breaches, to name a few.

Homeowner’s Policy Business Endorsements Versus Home-Based Business Insurance Policy

In some cases, carriers will offer a small business endorsement that can be added to a homeowner’s policy. This could add additional coverage for a small operation out of the home. However, keep in mind these types of endorsements might not properly cover the needs of the business. Larger businesses that need specialized coverage may need specific home-based insurance coverage.

Home-based business insurance policies can offer more diverse coverages with higher limits compared to a homeowner’s policy endorsement. Stand-alone policies typically provide better coverage for business equipment, liability, workers’ compensation and cyberattacks.

Cost of Home-Based Business Insurance

The cost of home-based insurance policies will vary based on the type, size, and risks associated with the business, and the types of purchased coverages.

Agent to the Rescue

Once the business owner understands the important differences between a homeowner’s policy and coverage for a home-based business, SeibertKeck can help determine what coverage best suits your needs. To do this, we need to thoroughly understand your business and the industry in which you operate.

Important questions to consider:

- Do clients visit the home/property to conduct business?

- Does the business have inventory or supplies on the premises?

- How many employees does your business have and from where do they work?

- Does your business require a vehicle?

- Does your company have technology that stores clients’ personal or financial information?

- What might be unique risks your business could face?

SeibertKeck Insurance Partners can assist to determine the proper coverage for your business! Contact us today at 330-867-3140 and ask to speak to a business agent. You may request a quote below!