Call Us Today (800) 229-5266

Source: NPR

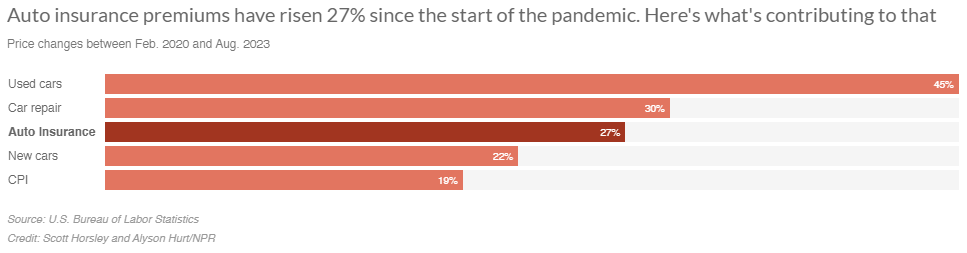

It’s not only car prices that are giving drivers sticker shock these days — it’s also happening when they open their car insurance bills. The cost of auto insurance jumped more than 19% during the year ending in August, while overall inflation was 3.7%, according to the Labor Department Wednesday.

On a monthly basis, car insurance prices rose 2.4% between July and August, contributing to a larger than expected jump in core inflation for the month. Inflation was also fueled in August by rising rents and gasoline prices.

Here are four reasons driving the spike in car insurance prices — and what car owners can do to save money.

Drivers have gotten a lot riskier during the pandemic

Insurance premiums actually fell in the early, locked-down stage of the pandemic when many cars sat parked for weeks. By they time they returned to the roads, however, many drivers seemed to have forgotten how to drive safely. “People picked up some risky habits,” says Sean Kevelighan, CEO of the Insurance Information Institute. “And we haven’t seen those risky habits go away, even though we have more people on the road.”

The number of fatal auto accidents jumped sharply in late 2020 and early 2021, according to the National Highway Traffic Safety Administration. While accident rates have since declined, they remain higher than they were before the pandemic, which contributes to the rising cost of insurance.

Repairs and parts replacements are proving costly

The cost of repairing or replacing a car that’s damaged in an accident have also jumped sharply, thanks to snarled supply chains, parts shortages and a tight labor market that’s led to rising wages for auto mechanics. New and used car prices have begun to fall in recent months, but repair costs are still climbing.

“As much as we’re beginning to see month over month decreases in inflation, which is good news, we also have to set in there that we have seen pretty significant price increases overall that have taken place over the last three years,” Kevelighan says.

Natural disasters are also driving up insurance costs

In addition to car crashes, natural disasters — fueled in some cases by climate change — are also contributing to higher insurance premiums, and not just in states prone to hurricanes or wildfires.

“We see a lot of hail damage,” says Grace Arnold, who oversees Minnesota’s insurance market as the state’s Commissioner of Commerce. Arnold says the costs of weather occurrences can quickly add up.

“We consistently have billion-dollar storms in Minnesota, even if they don’t have the 24-hour hurricane watch ahead of them,” she adds.

Insurance regulators have to strike a balance

Regulators like Arnold have dual role: trying to keep insurance premiums low enough for drivers to afford them while also keeping insurance companies solvent, so they can keep paying claims.

“We in general have found that the rate increases are justified” she says, by the higher costs that insurance companies are facing.

The Insurance Information Institute says auto insurers paid $1.12 in claims last year for every dollar they collected in premiums. This year, that ratio is expected to be $1.09. Insurance companies typically count on investment proceeds to cover that shortfall.

“What people really don’t understand is that insurance companies make most of their money by investment of our premiums,” says Harvey Rosenfield, the founder of Consumer Watchdog in California. “When they run into trouble, they have a scapegoat system set up where they blame something else for the fact that they need to raise their rates because they want to offset their investment losses. That’s how the industry works.”

So what can you do?

Most states require drivers to carry auto insurance, but there are ways for drivers to lower their costs. “The very first thing you’ve got to do is shop around,” Rosenfield says. “There are often better deals to be had.”

Many companies offer a discount for drivers who bundle their auto and home insurance, as TV commercials seem to tout all the time. Others will lower the premium for drivers who agree to install an app on their phone, allowing the company to track their driving habits.

Opting for a higher deductible can lead to lower premiums, though Arnold cautions against gambling with too little insurance. “I find it helpful to think through a couple of examples,” she says. “If I had my car stolen, what would that mean for me? If I were in an accident, what would that mean? The last thing you want is to be surprised.”

Arnold says her office gets some complaints about the jump in auto insurance premiums. But more often she hears from people who are unhappy with what they see as a skimpy payout when they file a claim.